Consent Mode v2 Unified Control (June 15, 2026): Why Financial Services Can't Ignore This

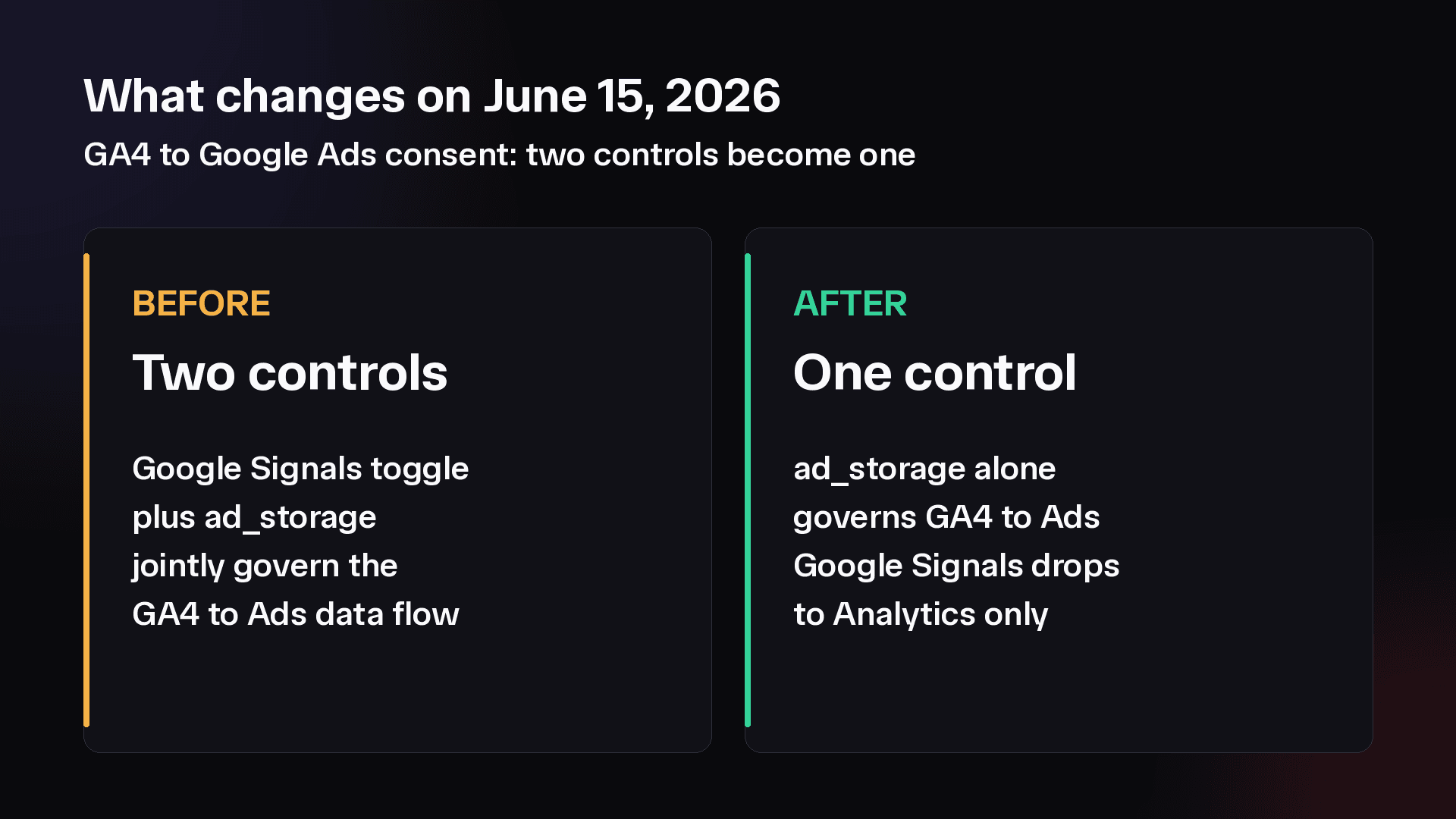

On June 15, 2026, a critical change takes effect in Google Consent Mode v2: the ad_storage consent control becomes the single governing signal for whether GA4 sends data and identifiers to Google Ads. Before June 15, this was controlled jointly by the GA4 "Google Signals" toggle and the ad_storage setting. After June 15, only ad_storage matters. For companies handling loan applications, credit decisions, and payment methods, a mismatch between consent banners and actual data collection is a direct regulatory risk under GDPR and 19 active state privacy laws. Full details from Google's official support documentation.

Most fintech companies treat GA4 consent as a proxy for overall consent architecture. After June 15, that assumption breaks. GA4 can signal "user consented to analytics" while Google Ads receives "user did not consent to ad storage" if your CMP is misconfigured. Meanwhile, Google Signals narrowing to Analytics-only means signed-in user association happens inside GA4 but does not automatically govern ad behavior. Regulators audit consent logs and compare them to actual tag behavior. A divergence is a violation.

Key takeaways

- On June 15, 2026, Google Ads stops reading Google Analytics 4 consent settings and relies entirely on CMP signals sent through Consent Mode v2 API.

- GA4 and Google Ads consent become completely independent. A misconfigured CMP can send conflicting signals to the two platforms.

- GDPR enforcement is active and escalates based on violation severity and scale. Nineteen US states now have comprehensive privacy laws. Most large fines relate to consent validation audits.

- Many fintech implementations use npa=1 (personalization disabled) instead of preventing collection. This creates an expectation mismatch: users expect no collection, but tags still fire.

- Fintech consent scenarios are higher risk: a user applying for a loan expects financial info doesn't flow to third-party analytics. Consent mismatch is a high-probability violation vector.

- Post-June 15, fintech must audit CMP config quarterly, comparing actual signal outputs to promises made in the consent banner and privacy policy.

The June 15 Shift: What Changes

Consent Mode v2 is a signaling protocol, not a tag blocker. It tells your platforms what the user consented to. Your CMP is responsible for implementing the actual blocking logic.

Before June 15, whether GA4 sends data and identifiers to Google Ads was governed by two controls: the GA4 "Google Signals" toggle AND the ad_storage setting. After June 15, only ad_storage controls this behavior. Google Signals narrows to Analytics-only, meaning it governs only the association of sessions with signed-in users inside GA4, not ad behavior. Additionally, later in 2026, the ad_personalization Consent Mode setting will exclusively control whether GA4 data is used for ads personalization in the Ads account.

The result: clearer but stricter signal separation. One platform can think the user consented. The other thinks they did not. Regulators see the log files and fine for the mismatch.

The Three Critical Gaps Fintech Must Audit

Gap 1: ad_storage Misconfiguration

A user rejects ad storage in your consent banner. Your CMP sends the "ad_storage denied" signal to GA4 correctly. But the same CMP has outdated Consent Mode v2 configuration that still sends "ad_storage = true" to Google Ads. Result: GA4 respects the rejection and stops sending data to Ads. But if tag-level collection still fires, you have collected data under a false promise. If a regulator subpoenas your consent logs and tag behavior, this divergence is a violation.

Gap 2: Outdated CMP Configuration

Most CMPs default to "deny all" when first installed. Teams that configured CMPs three years ago never updated them when privacy policies changed or new state laws launched. Indiana, Kentucky, and Rhode Island added comprehensive privacy laws January 1, 2026. If your CMP is still configured for the 16 states that existed in 2024, you're now under-collecting signals for the new three states.

Gap 3: Consent Banner Promises That Tags Don't Enforce

A common pattern: the consent banner says "analytics is optional." The privacy policy says "we ask for consent." But the tag configuration never actually blocks analytics. It fires with consent=false, collecting data anyway. Fintech regulators see this divergence (banner promise vs tag behavior) and fine for the discrepancy, not because consent was denied, but because the company lied about what it would do with the data.

A documented mismatch between what your banner promises and what your tags actually collect is a direct liability vector for fintech companies.

Why Fintech Is Higher Risk

Fintech consent scenarios carry higher regulatory scrutiny than most industries. A user applying for a loan expects that application data doesn't leak to Google's broader ad network. A user paying their credit card expects transaction metadata stays within the card issuer's ecosystem. Consent mismatch in these scenarios isn't just a policy violation. It's a customer expectation breach that regulators are actively auditing.

The cost of getting this wrong: GDPR fines escalate based on violation severity and scale. Most large enforcement actions relate to consent validation audits where regulators compare log files to promises made in consent banners and privacy policies. A documented mismatch between what your banner promises and what your tags actually collect is a direct liability vector.

"A user applying for a loan expects that application data doesn't leak to Google's broader ad network."

How to Audit Your Consent Architecture Post-June 15

Step 1: Map your current CMP output.

Extract the Consent Mode v2 signals your CMP sends for ad_storage to GA4 and Google Ads. Use Google Tag Manager's "Consent Overview" report to log what your CMP is actually sending. Log a sample of users who reject ad_storage consent. Verify that GA4 respects the rejection (doesn't send data to Ads). Verify that Google Ads also respects it (doesn't fire). If they diverge, document the gap.

Step 2: Compare signal output to banner promises.

Read your consent banner text. It says something like "Ad storage requires consent" or "Marketing cookies require consent." Now log what your CMP actually sends to each platform when a user rejects that category. If the banner says the data won't be sent to ads, but your CMP sends ad_storage=true anyway, that's a violation.

Step 3: Check CMP configuration against current privacy laws.

Your CMP was probably configured for GDPR plus the 16 state privacy laws that existed when you set it up. Verify it accounts for Indiana, Kentucky, and Rhode Island's comprehensive privacy laws (effective January 1, 2026). Different states have different opt out mechanisms. Indiana allows a single "universal opt out preference" signal. Rhode Island requires affirmative consent per cookie category. Misconfiguring for a single jurisdiction that expanded its scope is a common violation vector.

Step 4: Set up quarterly signal reconciliation.

Post-June 15, set a 30-day calendar reminder to audit CMP configuration. Every time Google publishes a policy update (2-3 times per month), check whether it affects your consent architecture. Every time a new state law takes effect, verify your CMP accounts for it.

Audit Your Consent Architecture

Fintech consent mismatches create direct GDPR and state privacy violation risks. Our compliance strategy team helps you map CMP signals, align banner promises to tag behavior, and document what you're actually collecting.

Start Your Consent AuditFrequently Asked Questions

June 15, 2026 is not a deadline for new compliance. It's the date that an existing mismatch becomes auditable. Many fintech companies already have divergent consent signals. They haven't been caught because regulators haven't looked yet. The consolidation on June 15 makes the divergence visible in the logs and creates an audit trail that regulators can follow. Audit your CMP configuration before then, align banner promises to tag behavior, and document what you're actually collecting. For fintech PPC strategy and policy baseline, see our 2025 Google Ads Safety Report. For a deeper look at how to architect fintech accounts for compliance across multiple regions, see our compliance-first PPC guide. To discuss consent architecture for your fintech platform, contact our compliance strategy team.

Kuba Strugarek

CEO & Co-founder of Oligamy Marketing, also a CMO for Oligamy Software activities. Built offline conversion tracking that delivered 536% YoY growth in Latin America. Performance Marketing on regulated markets.