We Reduced a Lending Company CPA by 84%. Here's the Infrastructure.

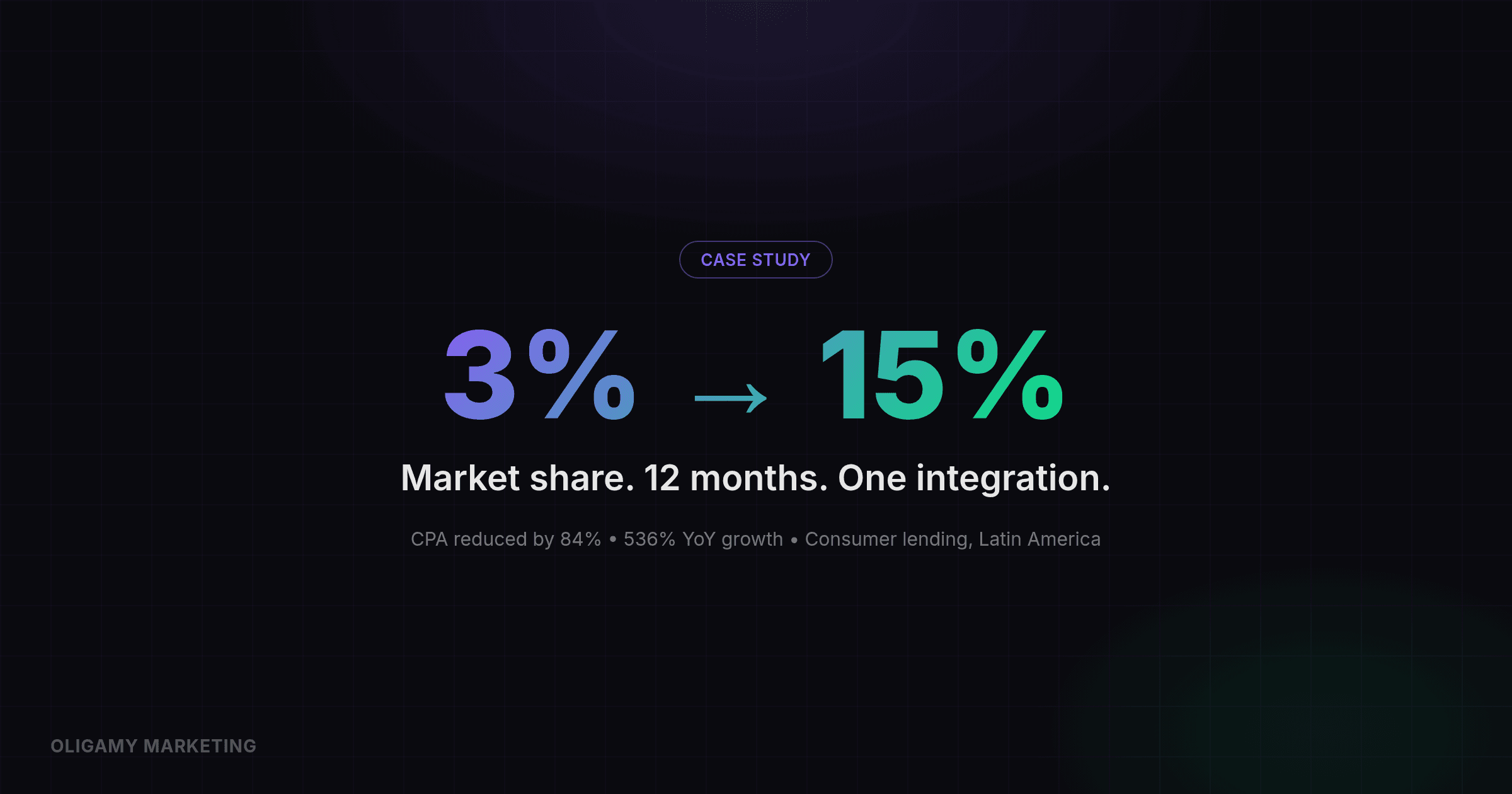

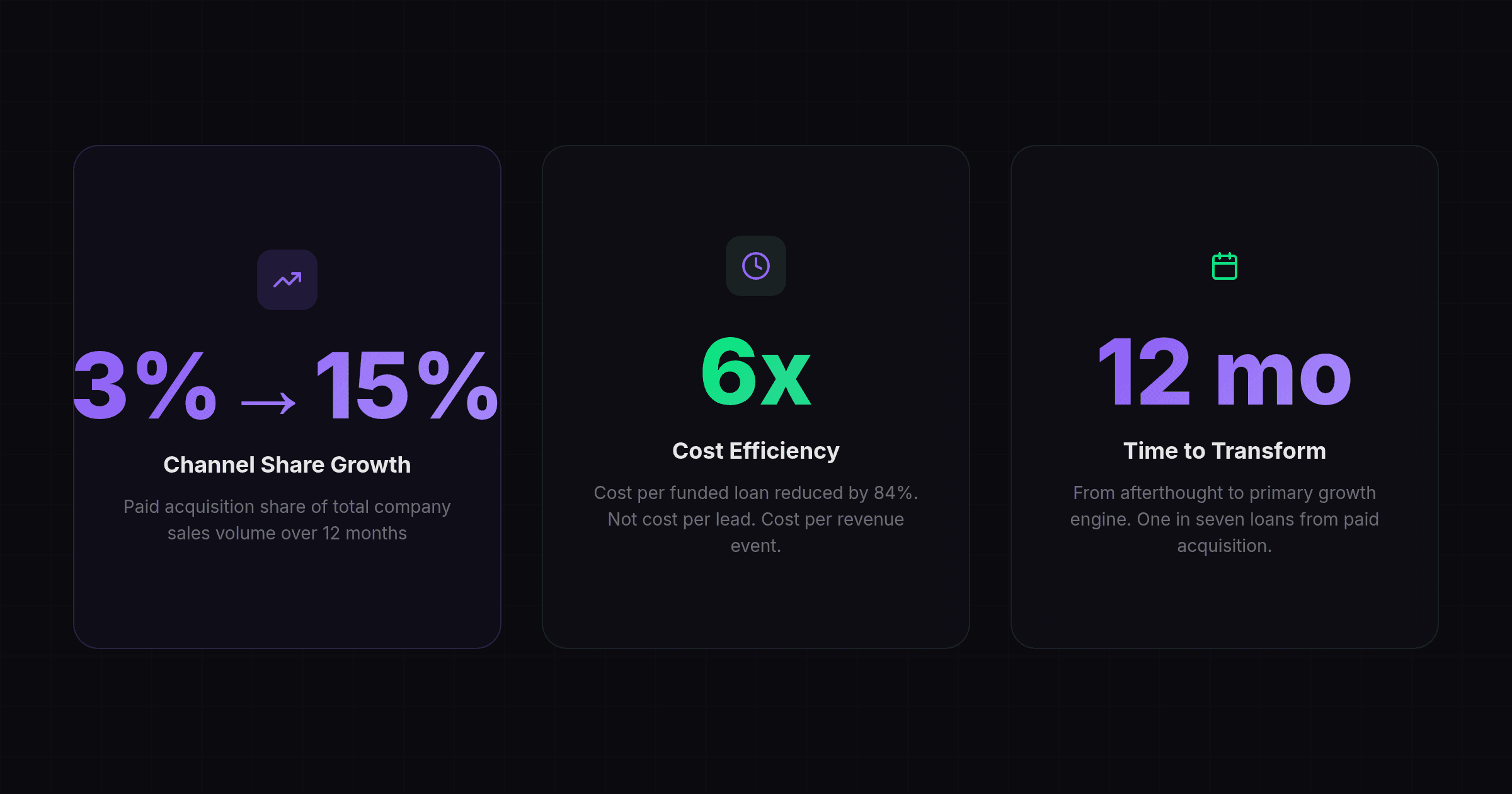

536% YoY growth. 84% lower cost per funded loan. Market share from 3% to 15%. Twelve months. One integration.

This is not a projection. It is not a benchmark from a Google whitepaper. These are the actual numbers from a consumer lending client in Latin America where Oligamy Marketing rebuilt the measurement infrastructure from scratch.

Offline conversion tracking is the process of sending conversion data that occurs outside the browser, inside a CRM or loan management system, back to ad platforms like Google Ads so that bidding algorithms can optimize on real business outcomes instead of proxy metrics like form submissions.

The core of the transformation was a single technical decision. Stop optimizing Google Ads for form fills and start optimizing for funded loans. That required connecting the client CRM to Google Ads via the API, feeding actual loan disbursement data back into the bidding algorithm, and switching from target CPA to target ROAS on real revenue events.

Everything else followed from that.

This fintech PPC case study breaks down the infrastructure, the implementation timeline, the results month by month, and what this approach looks like in 2026 with Enhanced Conversions for Leads and the Data Manager API.

The Problem - What 3% Market Share Actually Looks Like?

When we started, the client paid acquisition channel was a rounding error. Three percent of total company sales. The internal conversation was not about scaling. It was about shutting down paid media.

The Google Ads account looked healthy on paper. Cost per lead was stable. Click through rates were above benchmarks. The agency managing the account reported positive trends every month.

But cost per lead is not cost per customer.

The lending funnel has six to eight stages between a form fill and a funded loan. Credit checks. Document verification. Underwriting. Compliance review. Disbursement. Google Ads could see the form fill. It could not see anything after that.

Smart Bidding was doing exactly what it was told to do. It optimized for form submissions. It learned to find people who fill out forms. That is a fundamentally different audience than people who get approved, funded, and repay loans profitably.

The result? campaigns attracted form fillers, not borrowers. Conversion rates from lead to funded loan hovered around 8%. The actual cost per funded loan was roughly 5x what the dashboard showed as "cost per conversion."

The algorithm was not broken. It was blind.

When Google Ads Smart Bidding optimizes for form fills instead of funded loans, the actual cost per customer can be five times higher than the dashboard reported cost per conversion.

The Infrastructure We Built

Fixing this required three connected changes. None of them works alone. A CRM integration without value based bidding is a data pipeline to nowhere. VBB, without offline conversion data is optimizing on fiction. And both without compliance controls will get your account suspended in a regulated market within weeks.

Connecting the CRM to Google Ads

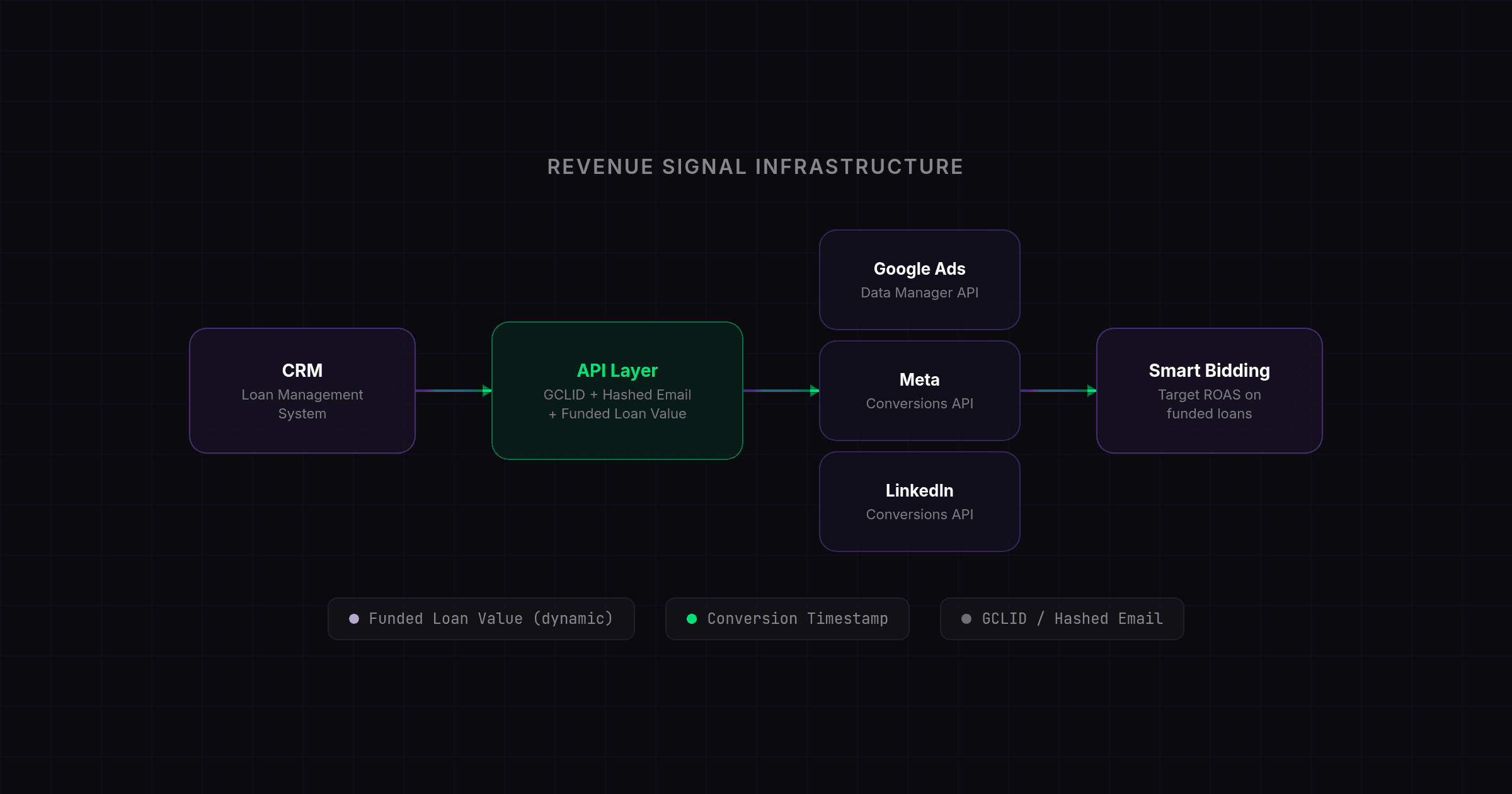

The foundation of everything was a custom API integration between the client loan management platform and Google Ads.

Every time a user clicked a Google ad, we captured the GCLID (Google Click Identifier) on the landing page and stored it alongside the lead record in the CRM. When that lead progressed through the funnel, from application to credit check to approval to funded loan, the CRM triggered an API call back to Google Ads with three pieces of data..

- original GCLID,

- conversion event type,

- actual funded loan amount in the local currency.

Imported four conversion events at different funnel stages:

- Application Completed. High volume, fast signal. Gave Smart Bidding early directional data within 24 to 48 hours of the click.

- Loan Approved. Medium volume. Strong quality signal. Occurs 3 to 14 days after application depending on the product and market.

- Loan Funded. This was the primary optimization target. The actual revenue event. Dynamic value: the real funded amount in local currency.

- First Repayment Low volume, but the ultimate quality signal. A funded loan that gets repaid is worth more than one that defaults. This event carried a lifetime value multiplier.

The integration ran on automated daily uploads initially, then moved to hourly as volume scaled. The API partial failure handling ensured that one malformed record (expired GCLID, timestamp outside the conversion window) never blocked the entire batch.

This was not a Zapier connection. The client lending platform had custom data structures, multi currency requirements, and compliance driven data handling rules that made off the shelf connectors insufficient. A custom build was the only viable path.

Switching to Value Based Bidding

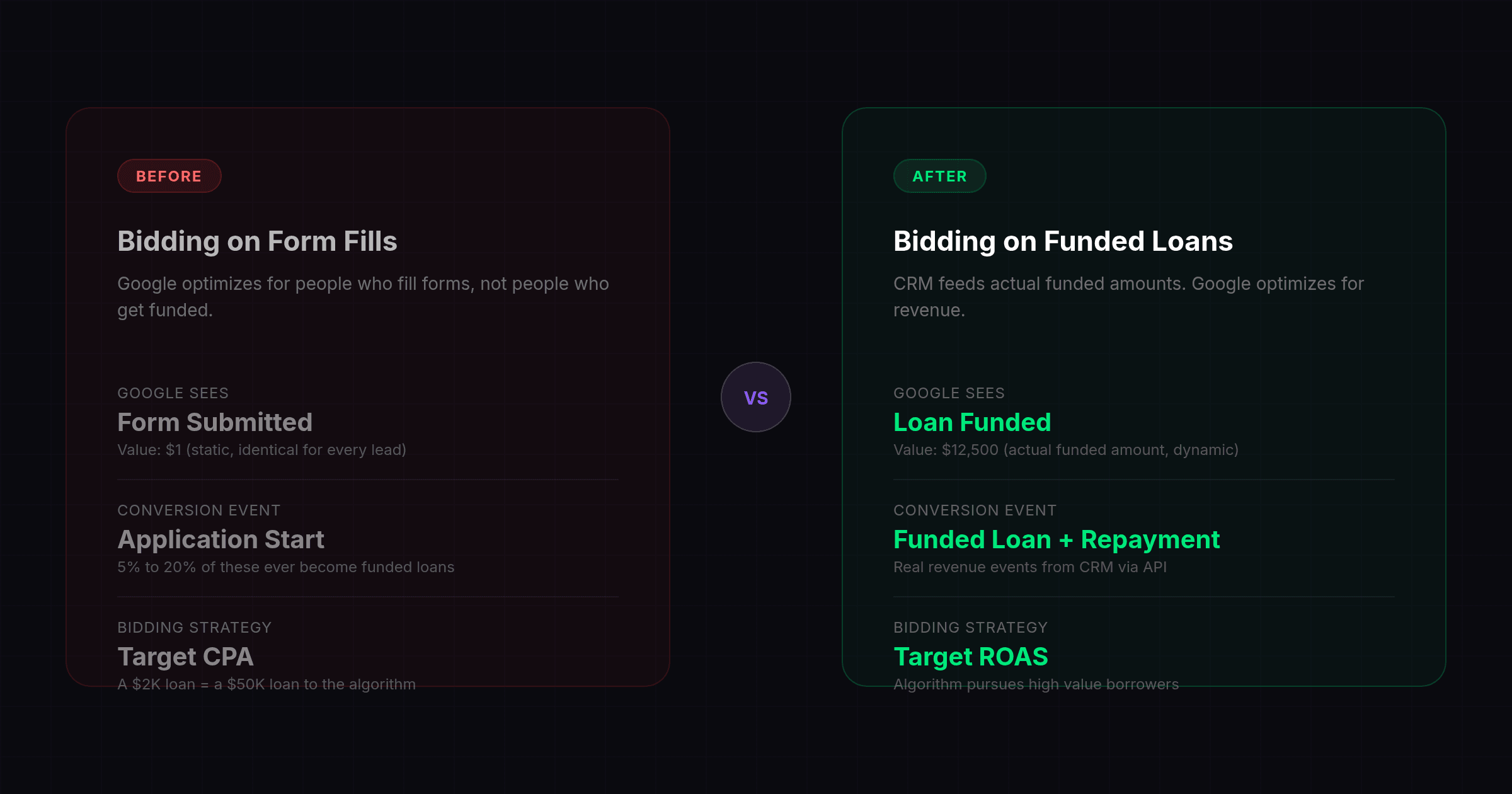

With funded loan data flowing into Google Ads, we could make the most important change: moving from target CPA to target ROAS.

Target CPA tells the algorithm:

get me conversions at a fixed cost.

A loan worth 5,000 and a loan worth 50,000 cost the same to acquire. The algorithm treats them identically. It has no reason to prefer one over the other.

Target ROAS tells the algorithm:

maximize total conversion value at a given return.

Now the system actively pursues clicks likely to produce high value funded loans. It bids more on users whose signals match historical high value borrowers.** It bids less on profiles that convert but at low amounts**.

Switching from target CPA to target ROAS on funded loan values was the single largest performance lever in the entire engagement, responsible for the majority of the 84% CPA reduction.

We did not flip the switch overnight. Before migrating, we uploaded 90 days of historical offline conversion data with accurate values and timestamps. This gave the algorithm a baseline from day one instead of forcing it to learn from zero.

Then we ran parallel campaigns: 30% of budget on target ROAS, 70% on existing target CPA. Over eight weeks, as the ROAS campaigns stabilized and demonstrated lower cost per funded loan, we progressively shifted budget. By week 12, the full account ran on value based bidding.

The Compliance Layer

In regulated lending markets, one non compliant ad can suspend an entire account. A suspended account in your primary growth channel is not an inconvenience. It is a revenue stop.

Across five regulated markets and 12 months of aggressive scaling, we maintained zero policy violations. Zero account suspensions. Zero compliance incidents.

We were the one, doing emergency meetings, and fixing account violations after multiple agencies.

This was not luck. It was architecture. The account structure behind compliant scaling across multiple regulated markets is its own discipline, and we break it down in our playbook for launching paid media in new regulated regions.

Every ad creative went through a four step compliance framework before going live:

- Regulatory mapping. Identifying which regulations applied in each specific market. Google Ads financial services policy is the baseline, but each country layers additional requirements. APR disclosure rules differ between jurisdictions. Keyword restrictions vary. What passes review in one market triggers a flag in another.

- Keyword filtering. Building negative keyword lists and creative exclusions specific to each market's regulatory environment.

- Creative adaptation. Adjusting ad copy, landing page disclosures, and legal text per market. Not translating. Adapting for local regulatory requirements.

- Pre launch review. Every campaign went through internal compliance review before activation. No exceptions. This added 2 to 3 days to launch timelines. It also meant zero violations in 12 months.

What Actually Happened? Month by Month

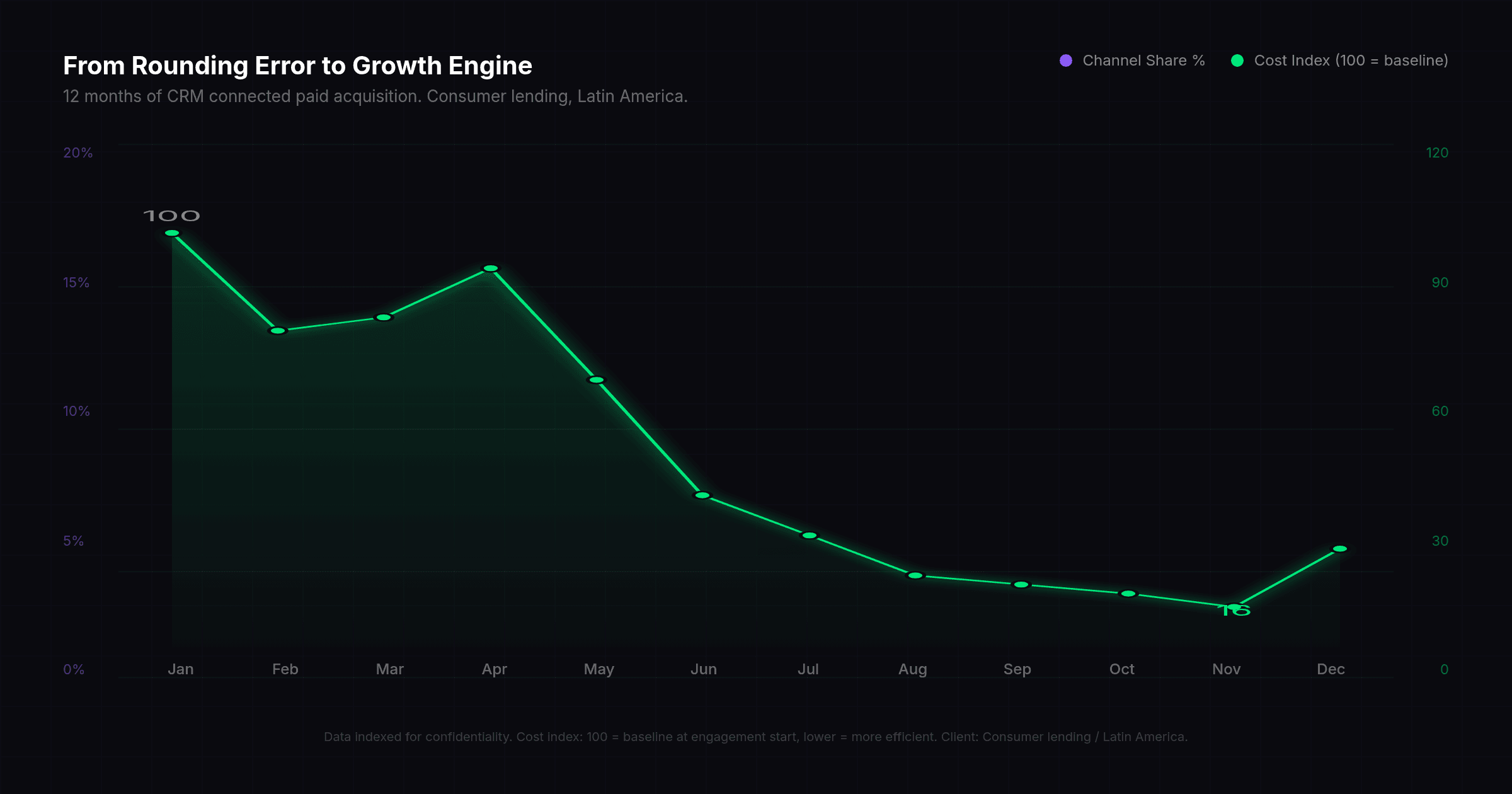

The transformation was not linear. Month 3 was worse than month 1 on several metrics. The learning period for value based bidding introduced volatility. Here is what the data actually looked like.

Months 1 to 3 - Infrastructure and learning.

January started at 3% channel share with a cost index of 100 (baseline). February held steady at 3% share, but cost dropped to 78 as we cut the worst performing campaigns. March showed a spike to 6% share, but April actually regressed to 4% with cost climbing back to 92. This was the value based bidding learning period. The algorithm was recalibrating. Stakeholders got nervous. We expected this.

Months 4 to 6 - Inflection point.

May hit 5% share with cost at 67. June was the turning point. 7% share, cost at 41. The algorithm had enough conversion data to start making consistently better bid decisions. From this point forward, every month improved.

Months 7 to 9 - Acceleration.

July crossed 10% share with cost at 32. August reached 13% at cost index 23. September held at 13% with cost continuing to fall to 21. The system was now beginning to stable itself, better data produced better bids, which produced more funded loans, which produced better data.

Months 10 to 12 - Dominance.

October hit 14% share at cost index 19. November peaked at 15% share with the lowest cost of the entire engagement: index 16. December settled at 15% share with cost ticking up slightly to 29 as we expanded into new market segments.

The final scorecard from Oligamy Marketing 12 month engagement...

- 536% YoY growth, in funded loan volume from the paid channel.

- 84% reduction, in cost per funded loan. Not cost per lead. Cost per actual revenue event.

- Market share from 3% to 15%, The paid channel went from an afterthought to the company primary growth engine. One in seven loans came from paid acquisition, up from one in thirty three.

- Zero compliance violations, across five regulated markets throughout the entire engagement.

- 100% success rate in restriction applies, for other agencies related policy violations

One detail that often surprises people, cost per lead actually increased during this period. The dashboard metric that most agencies optimize for went in the "wrong" direction. But cost per funded loan, the metric that appears on the P&L, dropped 84%.

Google was spending more per click, on clicks that converted into funded loans at dramatically higher rates. This is a pattern Oligamy Marketing has observed consistently while optimizing for the right conversion event may make surface metrics look worse while making the business metrics dramatically better.

What This Infrastructure Looks Like in 2026

The implementation that Oligamy Marketing built used Google Ads API , which was the standard approach at the time of the engagement. The landscape has shifted since then. If we were building this from scratch today, three things would be different.

ConversionUploadService

Enhanced Conversions for Leads

(ECL) as the primary signal path. Google now recommends ECL over legacy GCLID only imports. ECL supplements click identifiers with hashed first party data (email, phone number) captured by a Google tag at form submission. This recovers conversion signal from users who switch devices, clear cookies, or use iOS browsers where tracking parameters get stripped. According to Google, advertisers using ECL see a median 10% increase in measured conversions compared to GCLID alone. The best practice today is running both simultaneously: GCLID for maximum match accuracy, ECL as a fallback for signal loss. One important limitation: ECL has a maximum conversion attribution window of 63 days, compared to 90 days for standard GCLID based imports.

instead of

ConversionUploadService

Google Data Manager API (generally available since December 2025, currently at version 1.5 as of Q1 2026) is the recommended path for new offline conversion implementations. It does not require a developer token, supports encryption and confidential matching, and uses project based quotas.

Google official documentation now explicitly states:

We don't recommend implementing new offline conversion workflows using the Google Ads API.

ConversionUploadService still functions with no announced sunset date, but new builds should use Data Manager API IngestEvents method.

Multi platform by default. Meta discontinued their Offline Conversions API in May 2025. All offline event data now goes through Meta Conversions API (CAPI). LinkedIn launched their own Conversions API in February 2025. According to LinkedIn, advertisers using CAPI in beta saw a 20% decrease in cost per action. Those combining CAPI with Qualified Lead Optimization saw a 39% decrease in cost per qualified lead. A modern revenue signal infrastructure sends CRM data to all three platforms through a unified pipeline, not three separate integrations.

The core principle remains identical - connect your CRM to your ad platforms so bidding algorithms optimize on real business outcomes. This has evolved. The architecture has not.

Who This Works For?

This approach is not universal. It works for companies where the conversion that matters happens outside the browser. Lending. Insurance. Fintech companies with long approval cycles. B2B SaaS with long sales cycles. Any business where the gap between a form fill and actual revenue is measured in days or weeks, not seconds.

This works when...

-

You have a CRM that reliably tracks the full customer journey from first touch to revenue event. If your sales team does not update deal stages consistently, the data feeding the algorithm will be incomplete. Garbage in, garbage out.

-

You spend enough on paid media to give the algorithm learning volume. Value based bidding needs roughly 50 conversions per month at the target conversion event to optimize effectively. Below that threshold, the learning period stretches indefinitely.

-

You operate in markets where you can legally pass user level conversion data back to ad platforms. GDPR, LGPD, and local regulations require valid consent and data processing agreements. Your pipeline must respect consent status. No consent, no upload. From June 15, 2026, Consent Mode v2 changes how consent signals flow from your site into Google Ads, which we cover in our Consent Mode v2 guide for fintech.

This does NOT work when...

-

Your sales cycle exceeds 90 days consistently. Google's maximum conversion window is 90 days. Deals that close after that deadline simply cannot be attributed. For enterprise B2B with 6 to 12 month cycles, you need intermediate conversion events (qualified lead, proposal sent, contract negotiated) as proxy signals within the window.

-

Your CRM data is unreliable. If funded loan records are entered manually with multi day delays, if deal values are approximated rather than actual, if pipeline stages are skipped, the algorithm receives noisy signals and makes noisy decisions.

-

You are spending under $5,000 per month on paid media. The infrastructure cost (build time, maintenance, monitoring) does not justify itself below a certain spend threshold. The math changes at higher volumes.

Key Takeaways

- Optimizing Google Ads for form fills instead of funded loans can inflate the actual cost per customer by five times or more in lending.

- The core infrastructure required to fix this is a CRM to Google Ads API integration that passes funded loan amounts and the original click identifier back to the bidding algorithm.

- Migrating from target CPA to target ROAS on funded loan values requires uploading at least 90 days of historical conversion data before switching, then running parallel campaigns for 8 to 12 weeks.

- In regulated lending markets, compliance controls must be built into the data pipeline from day one. Consent status must gate every conversion upload.

- Cost per lead may increase when you optimize for the right conversion event. That is expected. The metric that matters is cost per funded loan, and that is where the 84% reduction came from.

Frequently Asked Questions About Offline Conversion Tracking

What is offline conversion tracking and why does it matter for lending companies?

Offline conversion tracking is the process of sending conversion data from your CRM or loan management system back to ad platforms like Google Ads. For lending companies, the conversion that matters (a funded loan) happens days or weeks after the ad click, inside internal systems that Google cannot see. Without offline tracking, the bidding algorithm optimizes for form fills instead of funded loans. Oligamy Marketing's implementation of this approach reduced cost per funded loan by 84% in 12 months for a consumer lending client in Latin America.

How long does it take to implement offline conversion tracking?

A complete implementation typically takes 8 to 12 weeks from audit to full migration. Weeks 1 to 4 cover funnel mapping, GCLID capture setup, and historical data extraction. Weeks 5 to 8 cover the API build, testing, and initial data uploads. Weeks 9 to 12 cover parallel bidding tests (target CPA versus target ROAS) and progressive budget migration. You should expect 1 to 2 weeks of bidding volatility during the transition as the algorithm learns from the new conversion data.

What is the difference between Enhanced Conversions for Leads and legacy offline conversion import?

Legacy offline conversion import relies solely on the GCLID (Google Click Identifier) to match CRM conversions back to ad clicks. Enhanced Conversions for Leads (ECL) adds hashed first party data (email, phone) as an additional matching signal. ECL recovers conversions from users who switch devices, clear cookies, or use browsers that strip tracking parameters. Google reports a median 10% increase in measured conversions with ECL. The recommended approach in 2026 is running both simultaneously, using GCLID for maximum match accuracy and ECL as a fallback.

What results can we expect from switching to value based bidding?

Google reports a median 14% increase in conversion value when switching from target CPA to target ROAS. Oligamy Marketing's lending case study saw 536% YoY growth and 84% CPA reduction, which included the full infrastructure build alongside the bidding strategy change. According to the Pixis 2025 industry benchmark covering $996 million in Google ad spend, value based bidding approaches (target ROAS and maximize conversion value) now account for 48% of all ad spend, exceeding traditional CPA based approaches at 43%. Individual results depend on funnel depth, conversion volume, and market conditions.

Do you need a custom API integration, or can tools like Zapier work?

For lending and financial services companies, a custom API integration is typically necessary due to dynamic loan values, multi currency support, and compliance requirements. The client in this case study required a custom build because their lending platform had proprietary data structures that no off the shelf connector could handle. For simpler funnels with one or two conversion stages, stable values, and fewer than 500 conversions per month, connector tools like Zapier or LeadsBridge can work.

How does compliance affect offline conversion tracking in regulated markets?

Under GDPR, a SHA256 hashed email address is still classified as personal data (pseudonymization is not anonymization). Your CRM to ad platform pipeline must respect user consent status. That means storing consent alongside the GCLID, filtering uploads based on consent, and maintaining data processing agreements with Google and Meta. Across five regulated markets spanning EU, Latin American, and Baltic jurisdictions, Oligamy Marketing maintained zero compliance violations throughout the 12 month engagement. Compliance is not a separate workstream. It is built into the pipeline architecture. If you are evaluating who can build and run this in a regulated market, our guide on how to find a fintech compliance marketing partner covers the questions to ask.

Data indexed for confidentiality. Channel share shown as percentage of total company sales volume. Cost index: 100 = baseline acquisition cost at engagement start, lower = more efficient. Client: Consumer lending / Financial services. Market: Latin America. All metrics represent actual engagement results, not projections or benchmarks.

Related reading

Three deeper breakdowns from the same body of work:

- How to structure accounts before launch when launching paid media in new regulated regions.

- The forensic view of what actually triggers financial services ad disapprovals, drawn from 273 million restricted ads in a single year.

- What the 2025 Google Ads Safety Report signals for financial advertising in 2026, from approval timelines to verification drift.

Kuba Strugarek

CEO & Co-founder of Oligamy Marketing, also a CMO for Oligamy Software activities. Built offline conversion tracking that delivered 536% YoY growth in Latin America. Performance Marketing on regulated markets.