273M Restricted Ads: What Actually Triggers Financial Services Disapprovals

Google restricted 273.4 million financial services ads in 2025, and never published the violation breakdown. After auditing more than 20 financial services accounts, we keep seeing the same eight patterns drive 40 to 60 percent of suspensions. Here is what separates the accounts that survive from the 24.9 million that got suspended.

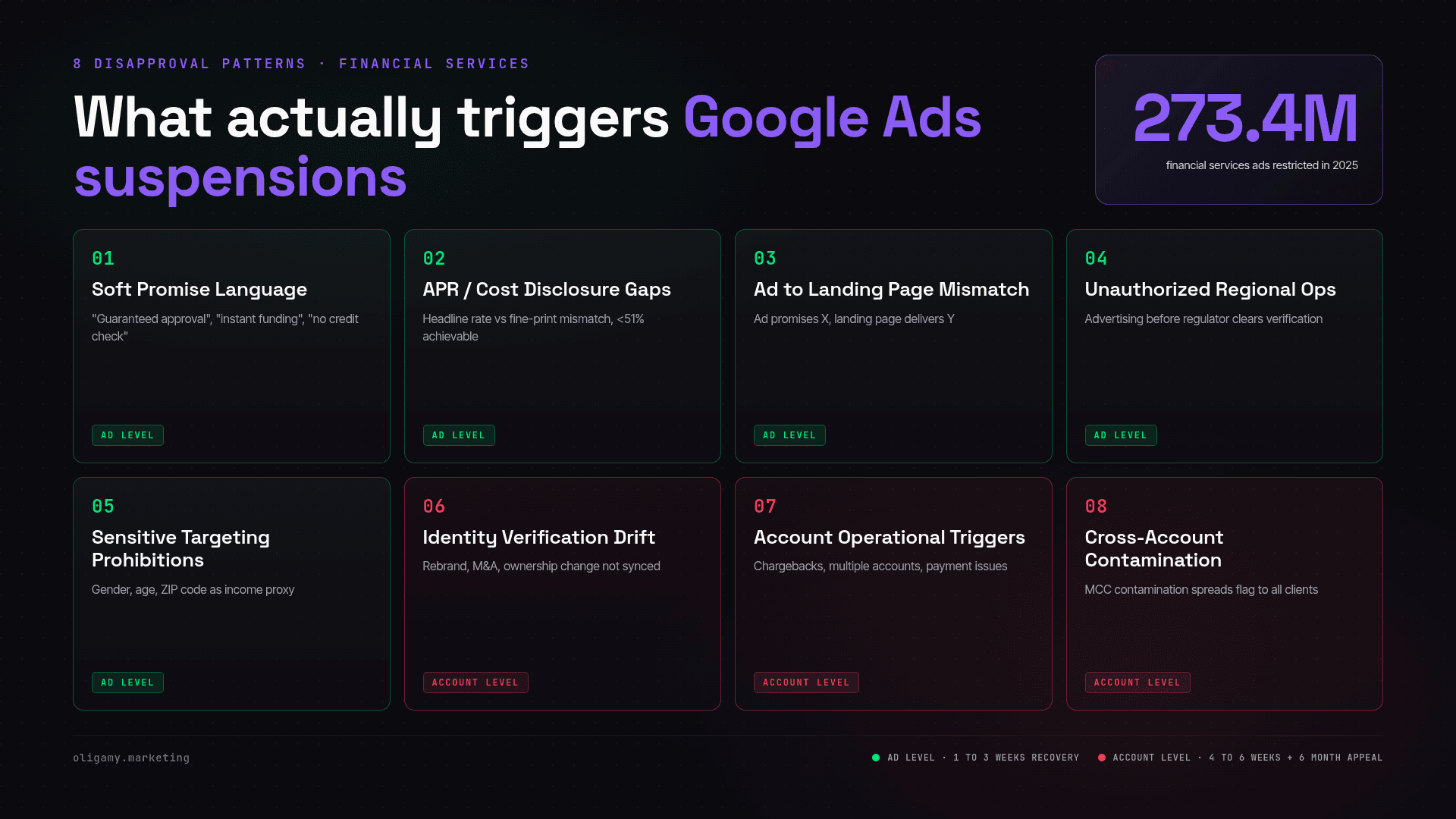

The 8 Patterns That Trigger Suspensions

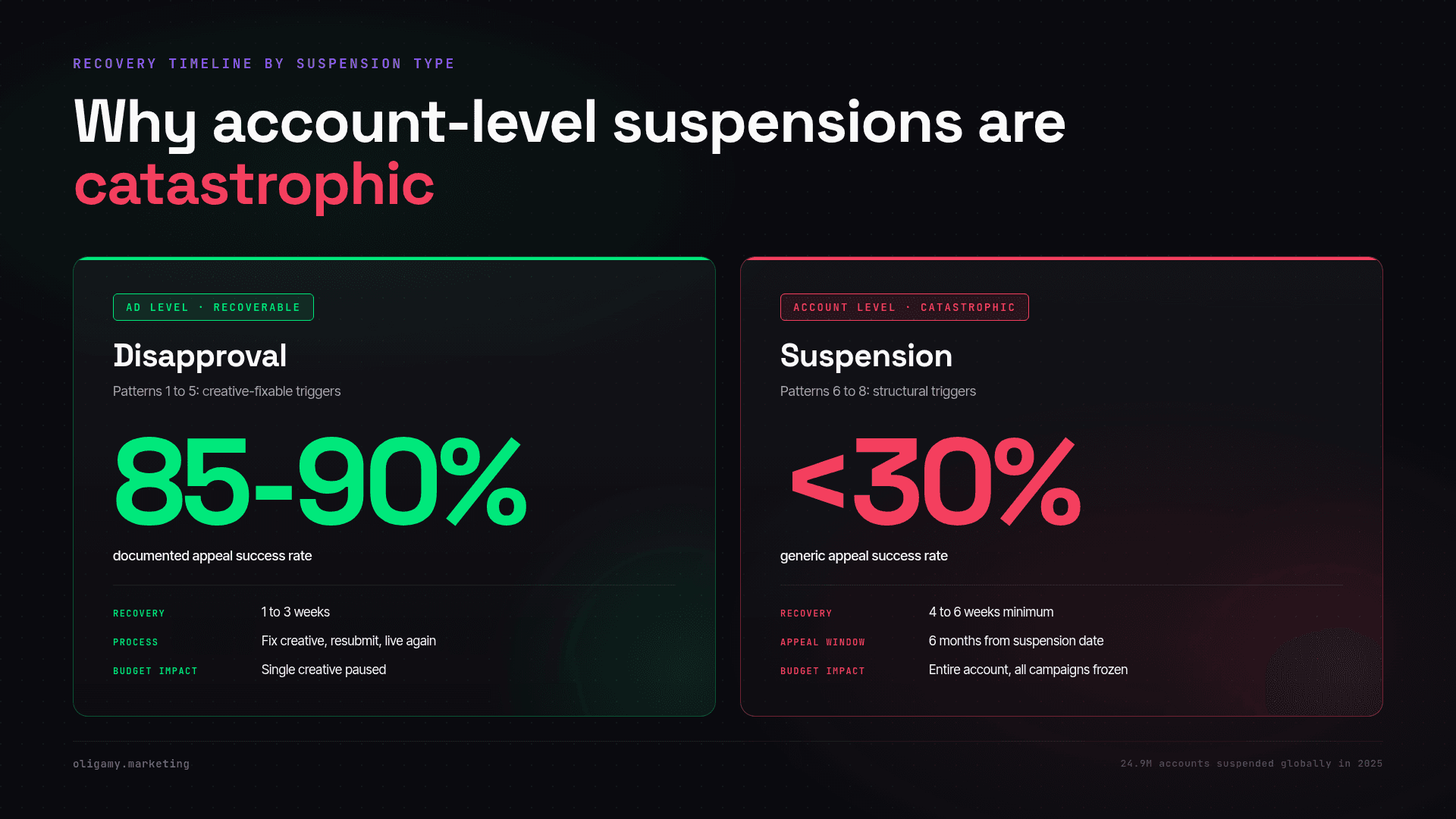

Patterns 1 to 5 are ad level, recoverable in 1 to 3 weeks. Patterns 6 to 8 are account level, which is catastrophic: 4 to 6 weeks minimum and a 6 month appeal window.

Pattern 1: Soft promise language. Claims like "guaranteed approval" or "no credit check" get disapproved if you cannot substantiate them for 100 percent of users. Use "See if you pre-qualify," "Decisions typically in 2 business days," or a plain "Apply now."

Pattern 2: APR and cost disclosure gaps. A headline that says "6% APR" with fine print that says "6 to 18%" is a violation. CCD2 requires the advertised rate to be achievable by at least 51 percent of approved applicants. Match the promise exactly.

Pattern 3: Ad to landing page misrepresentation. Ad says "up to $50K," the page says "up to $25K." Ad says "24 hour funding," the page says "5 to 7 days." Repeated mismatches escalate to account level flags.

Pattern 4: Unauthorized regional operations. Google checks verification status before publication. If you are not verified in a region, your ads block before launch. Do not launch until you have written confirmation from Google Ads that you are verified.

Pattern 5: Sensitive targeting prohibitions. Under the Google Ads financial services policy you cannot target by gender, parental status, or age, and you cannot use ZIP code as an income proxy. Use interest, behavior, or company targeting for B2B. Geo-targeting is safe.

Pattern 6: Identity verification drift. Your company rebrands, goes through M&A, or changes ownership, but the verified profile stays frozen. The next review cycle flags the mismatch. Any structural change needs a verification update in Account Settings within 10 days.

Pattern 7: Account level operational triggers. Behavioral red flags escalate you to manual review: repeated disapproval resubmissions (3 or more in 72 hours), declined payments, multiple accounts from one entity, chargeback patterns. A single trigger puts the whole account under heightened scrutiny.

Pattern 8: Cross account contamination through an MCC. One flagged account inside a Multi Client Container spreads the compliance flag to the entire MCC.

An agency managing 30 fintech clients under one MCC faces this every month: if client #5 violates, all 30 can freeze pending review. Separate your MCCs by risk tier (clean, watch list, high risk), or isolate high-risk clients under dedicated MCCs.

Ad Level vs Account Level: The Risk Difference

Patterns 1 to 5 are ad level disapprovals. Google rejects the ad, you fix it and resubmit, and you recover in 1 to 3 weeks. Patterns 6 to 8 are account level flags. Google suspends the entire account, stops every campaign, and halts budget flow.

An account level suspension gives you a 6 month appeal window. Properly documented appeals succeed 85 to 90 percent of the time. Generic ones succeed about 30 percent of the time. Since November 2025, Google resolves 99 percent of appeals within 24 hours, roughly 70 percent faster than the prior baseline.

The 24.9 million accounts suspended in 2025 were not creative quality issues. They were structural violations. For the cost-structure implications of this enforcement velocity, see our 2026 Google Ads Safety Report strategy guide.

The 5-Layer Pre-Suspension Audit

Most teams audit after suspension. Catch the violations before Google does.

Layer 1, creative language (1 to 2 hours). Search every ad for soft promises: guaranteed, instant, easy, no credit check. Does your data support each claim for 100 percent of users?

Layer 2, cost disclosure (2 to 4 hours per variant). For every ad with an APR, rate, fee, or term: is the full range in the headline? Is the advertised rate achievable by 51 percent or more of approved applicants? Are CCD2 and regional disclaimers present?

Layer 3, ad to landing page match (2 to 3 hours). Click 10 to 15 percent of active ads. Does the page offer match the ad promise exactly? Same disclaimers, same exclusions, same conversion definition?

Layer 4, identity verification (30 minutes). In Account Settings, confirm the company name, legal entity, and beneficial ownership are current. Any M&A or rebrand since verification? Update immediately.

Layer 5, MCC structure (1 to 2 hours planning). If you manage multiple fintech clients: separate accounts, isolated high-risk clients, no single point of contamination.

Total cost: 6 to 12 hours over 1 to 2 weeks. The cost of skipping it is an account suspension, 4 to 6 weeks of dead campaigns, and a 6 month appeal. Teams that run quarterly audits catch violations before account flags. Teams that do not discover them after suspension.

Why This Is Accelerating

Google published 35 policy updates in 2025, roughly one every 10 days, and financial services saw the most changes. AI enforcement is scaling too: 467 million web pages were actioned for violations in 2025, nearly 3 times the 2024 volume.

The 273M number is not shrinking. It is accelerating. Accounts that treat compliance as a quarterly checkbox usually survive until they do not. Accounts that treat it as infrastructure, with 30 day audits, constant verification maintenance, and creative guidelines applied at write-time, rarely get suspended.

This framework is built for Series A to C fintech, lending, and insurance companies running Google Ads in regulated regions. The real question is not whether you will hit a disapproval. It is whether it is an ad you fix in a week, or an account that suspends for 4 to 6 weeks.

Audit your account before Google does

We run the 5-layer pre-suspension audit on financial services accounts and rebuild the structure that keeps them live. Compliance as architecture, not a creative afterthought.

See our compliance strategyFrequently Asked Questions

Kuba Strugarek

CEO & Co-founder of Oligamy Marketing, also a CMO for Oligamy Software activities. Built offline conversion tracking that delivered 536% YoY growth in Latin America. Performance Marketing on regulated markets.